Bank of Upper Canada

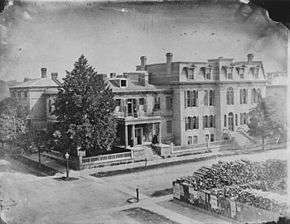

The Bank of Upper Canada Building in 1872 (Adelaide Street, Toronto) |

| |

| |

| |

| |

The Bank of Upper Canada was established in 1821 under a Charter granted by the legislature of Upper Canada in 1819 to a group of Kingston merchants.[1] This charter was "stolen" by the more influential Executive Councillors to the Lt. Governor, the Rev. John Strachan and William Allan and moved to Toronto. The bank was closely associated with the group that came to be known as the Family Compact, and formed a large part of their wealth. This association with the Family Compact and underhanded practices made Reformers, including Mackenzie, regard the Bank of Upper Canada as a prop of the Government.[2] Complaints about the bank were a staple of Reform agitation in the 1830s due to its monopoly and aggressive legal actions against debtors.[3]

Organization

Bank of the Family Compact

The first Bank of Upper Canada was located on the south-east corners of King and Frederick street in Toronto.[4] Toronto at the time was too small for a bank and its promoters were unable to raise even the minimal 10% of the £200,000 authorized capital required for start-up. The bank succeeded only because its promoters had the political influence to have this minimum reduced by half, and because the provincial government subscribed for two thousand of its eight thousand shares. The Lt. Governor appointed four of the bank’s fifteen directors making for a tight bond between the nominally private company and the state. Despite these tight bonds, the Receiver General, the reform leaning John Henry Dunn, refused to use the bank for government business.[5]

The bank’s principle promoters were the Rev. John Strachan, and William Allan. William Allan, who became president, was also an Executive and Legislative Councillor. He, like the Rev. John Strachan, played a key role in solidifying the Family Compact, and ensuring its influence within the colonial state. Forty-four men served as bank directors during the 1830s; eleven of them were executive councilors, fifteen of them were legislative councilors, and thirteen were magistrates in Toronto. More importantly, all 11 men who had ever sat on the Executive Council also sat on the board of the Bank at one time or another. 10 of these men also sat on the Legislative Council. The overlapping membership on the boards of the Bank of Upper Canada and on the Executive and Legislative Councils served to integrate the economic and political activities of church, state, and the “financial sector.” These overlapping memberships reinforced the oligarchic nature of power in the colony and allowed the administration to operate without any effective elective check. Henry John Boulton, the solicitor general, author of the bank incorporation bill, and the Bank's lawyer, admitted the bank was a “terrible engine in the hands of the provincial administration.”[6]

William Lyon Mackenzie, the Reform politician and newspaper publisher, was the first to demonstrate the nature of this oligarchic power by showing that the government, its officers, and legislative councilors owned 5,381 of its 8,000 shares. Once elected to the House of Assembly, he critiqued the Bank's lack of transparency and accountability to the legislature.

The "Pretended Bank" (at Kingston) and the Commercial Bank of the Midland District

The Bank of Upper Canada at York (Toronto) had obtained its charter at the expense of the larger, more economically developed town of Kingston. Deprived of their charter, they established an unchartered bank in 1818 supported with American capital. The government refused to accept its notes given its American ties, and it went bankrupt in 1822. After its failure, the Bank of Upper Canada used all of its influence to prevent any other bank from being chartered in the province. This monopoly was crucial to keeping its notes in circulation and boosting its profits. They succeeded only until 1832 when the Commercial Bank of the Midland District was chartered finally giving Kingston the bank it desired.[7]

Banknotes

Paper currency was a banking innovation in this era. It had been experimented with to fund the American Revolutionary War, but had devalued badly, leading to general distrust of banknotes. Banknotes in this period were not legal tender, issued by a state bank. They were, rather, similar to cheques written by the bank promising to pay the bearer with "real" (usually metallic) money, or specie, if they returned the cheque to the bank. Any bank which could not redeem its banknotes with specie was forced to close for good.

The Bank of Upper Canada was able to loan out many more banknotes than it had the cash to redeem because Upper Canada was a specie poor province, and the notes would pass from hand to hand to enable trade without ever being returned to the bank. On average the bank loaned out more than three times more banknotes than it could redeem; it made 6% interest on each note that it loaned out.

The bank’s manager, Thomas Ridout, estimated that in the first three years of its operation, the bank’s notes comprised between 74 and 77% of the province’s money supply. Between 1823 and 1837, its profit on paid in capital ranged between 3.6% (1823) and 16.5% (1832) at a time when the maximum legal interest rate was 6%.

The Bank of Upper Canada suspended payments from March 5, 1838 – November 1, 1839 during the financial panic of that year. It was bankrupt, but a special act of legislature allowed it to continue operating without having to repay its loans with specie.[8] The bank was a small operation which, like many early Canadian banks, collapsed in 1866.

Bank Officers

- William Allan (1822–1835)[9]

- William Proudfoot (1835–1861)[10]

- Thomas Gibbs Ridout, cashier (general manager) (1822–1861)

- Henry John Boulton, lawyer (1825-1833)

The directorate of the bank was dominated by government officers. Forty-four men served as bank directors during the 1830s; eleven of them were executive councillors, fifteen of them were legislative councillors, and thirteen were magistrates in Toronto.[6]

Joint Stock Competition

The financial panic of 1836-8

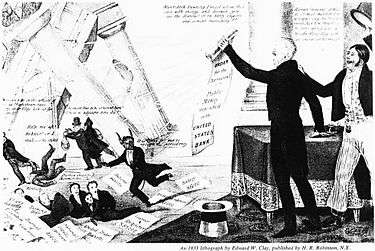

On 10 July 1832, President Andrew Jackson vetoed the bill for the rechartering of the Second Bank of the United States, arguing that it was utilized by a "moneyed aristocracy" to oppress the common man. This was the same complaint that the Reformers lodged against the Bank of Upper Canada, which served a similar role. The dismantling of the bank plunged the Anglo-American world into an enormous depression (1836-8) that was worsened by bad wheat harvests in Upper Canada in 1836. Farmers were unable to pay their debts. Most banks - including the Bank of Upper Canada - suspended payments (i.e. declared bankruptcy) by July 1837 and requested government support. While the banks received government support, ordinary farmers and the poor did not.

Bank Wars (1835-1838)

The Bank of Upper Canada was the subject of almost continuous political attack. Shortly after its founding, Reform critic William Lyon Mackenzie published a series of articles on how speculative the Bank's loan practices were, and how close to bankruptcy it was. This resulted in an event now known as the Types Riot in 1826, in which the clique of Bank officers dubbed the Family Compact destroyed Mackenzie's printing press. Mackenzie, a bank critic, pushed for a non-speculative "hard money" policy where the bank loaned out only the money it actually had.[11]

Until 1835, all banks in Upper Canada required a legislative charter. Reformers tried several legislative strategies to get their own bank, including attempts to incorporate credit unions such as the Farmers' Storehouse company. This came to an end in 1835 when Charles Duncombe produced a “Report on Currency” for the Legislative Assembly which demonstrated the legality of the Scottish joint-stock bank system in Upper Canada.

The difference between the English chartered banks and the Scottish joint stock banks is that the Scottish banks were considered partnerships and hence didn't need a legislated Act in order to operate. The joint stock banks thus lacked limited liability, and every partner in the bank was responsible for the bank’s debts to the full extent of their personal property. The chartered banks, in contrast, protected their shareholders with limited liability and hence from major loss; they thus encouraged speculation. The Scottish joint-stock banks followed a "hard money policy." They avoided speculative risk because if they failed, their shareholders were responsible for the full loss. Since the banks did not require a legislated charter, many more banks could be founded, and they were more competitive and freer from political influence and corruption.[12]

Duncombe's report opened the gate for many new competitive banks to enter the market - just as the entire Anglo-American financial system was coming apart at the seams in a financial panic lasting until after the Rebellions of 1837. The Bank of Upper Canada only survived due to its influence on government.

The joint-stock banks

Following Duncombe's report, the Farmers' Bank and the Bank of the People were founded on a joint stock basis, until the Family Compact conspired to make new ones illegal in 1838.

The end of monopoly

The monopoly of the Bank of Upper Canada had been slowly eroding with the chartering of the Commercial Bank, and then the joint-stock banks. The Act to outlaw further joint-stock banks in 1838 again tilted towards monopoly. However, in 1841 the Bank of Montreal, long seeking an entry into Upper Canada, purchased the Bank of the People and quickly began to expand its branch network. The Bank of British North America also entered the provincial market at this time.

As a result, the Bank changed its strategy and in 1850 it became the official bank of the Province of Canada, collecting all government revenue and issuing all government cheques.[13]

Architecture

The building which housed the bank, constructed in 1825, still exists in Toronto's Adelaide St East and has been designated a National Historic Site of Canada. Designed by architect William Warren Baldwin, 1825–27, the bank resembled a London townhouse with a Doric portico.[1] The Bank of Upper Canada in Port Hope, Ontario built in 1857 is on the Registry of Historical Places of Canada.[14] The Bank of Upper Canada building in Toronto, Ontario built in 1827 to 1834 is on the Registry of Historical Places of Canada.[14] The former Bank of Upper Canada Building in Goderich, Ontario built in 1863 is on the Registry of Historical Places of Canada.[14]

Further reading

Baskerville, Peter. The Bank of Upper Canada: A Collection of Documents. Toronto: Champlain Society Publications, 1987.

Gallery

-

Bank of Upper Canada

-

Bank of Upper Canada 1977 condition

References

- 1 2 http://www.thecanadianencyclopedia.com/index.cfm?PgNm=TCE&Params=A1ARTA0000502 Bank of Upper Canada

- ↑ Peppiatt, Liam. "Chapter 80: Bank of Upper Canada". Robertson's Landmarks of Toronto Revisited.

- ↑ Baskerville, Peter (1987). The Bank of Upper Canada: A Collection of Documents. Toronto: Champlain Society. pp. xxvii–lxxiv.

- ↑ Peppiatt, Liam. "Chapter 7: First Bank in Upper Canada". Robertson's Landmarks of Toronto.

- ↑ Baskerville, Peter (1987). The Bank of Upper Canada: A Collection of Documents. Toronto: Champlain Society. pp. lxxii.

- 1 2 Schrauwers, Albert (2010). "The Gentlemanly Order & the Politics of Production in the Transition to Capitalism in the Home District, Upper Canada". Labour/Le Travail. 65 (1): 22–25.

- ↑ Baskerville, Peter (1987). The Bank of Upper Canada: A Collection of Documents. Toronto: Champlain Society. pp. lvi–lviii.

- ↑ Pound, Richard W. (2005). 'Fitzhenry and Whiteside Book of Canadian Facts and Dates'. Fitzhenry and Whiteside.

- ↑ "Upper Canada Rebellion 1837: The End". Sg-chem.net. 2000-01-01. Retrieved 2012-03-12.

- ↑ Peter A. Baskerville. "Bank of Upper Canada". The Canadian Encyclopedia. Retrieved 2012-03-12.

- ↑ Schrauwers, Albert (2009). Union is Strength: W.L. Mackenzie, the Children of Peace, and the Emergence of Joint Stock Democracy in Upper Canada. Toronto: University of Toronto Press. pp. 79–85.

- ↑ Schrauwers, Albert (2009). Union is Strength: W.L. Mackenzie, the Children of Peace and the Emergence of Joint Stock Democracy in Upper Canada. Toronto: University of Toronto Press. pp. 154–5.

- ↑ Baskerville, Peter (1987). The Bank of Upper Canada: A Collection of Documents. Toronto: Champlain Society. pp. cgi–cvii.

- 1 2 3 "Archived copy". Archived from the original on 2012-03-08. Retrieved 2010-05-07. Bank of Upper Canada

| Wikimedia Commons has media related to Bank of Upper Canada. |